Budget: How to Schedule Your Expenses

- Bubba Miller

- 3 days ago

- 4 min read

Budget: Scheduling

In order to have an effective budget, you have to be able to know what you can and cannot afford. Sounds simple, right? Of course it is simple. All of us can do basic elementary math. If I have $150 in checking, but the light bill is $200, I am going to need to move money over from savings to cover that deficit. But a successful budget should not have me pulling from my savings account, but rather I should have a plan to have that $150 for the light bill already in my account.

A budget can only be successful if the user is intentional. Furthermore, a budget and tracking your expenses are two different things. A budget is not just tracking your expenses, by my definition, because there is no net gain. By net gain, I mean, there is money left over at the end of the month from the income made. If I were to bring in $3,500 but spent $4,000, I was not budgeting but rather tracking my expenses. And if I was budgeting, I did not do a very good job. Budgeting is only successful if the user(s) are intentional in what they are spending.

This leads me into the scheduling section of budgeting. Money can do two things in a checking account. It can go in(flow) and it can go out(flow). But a problem that a lot of people run into is their inflows do exceed their outflows, and they end up taking out a credit card to make up the difference and this cycle continues and then poof! You have credit card debt that cannot be paid off because you were subsidizing your irresponsible spending with credit cards and there is no margin remaining to pay off debt. It is a vicious cycle. It is such a vicious cycle that consumers in the USA have $1.9T in credit card debt.

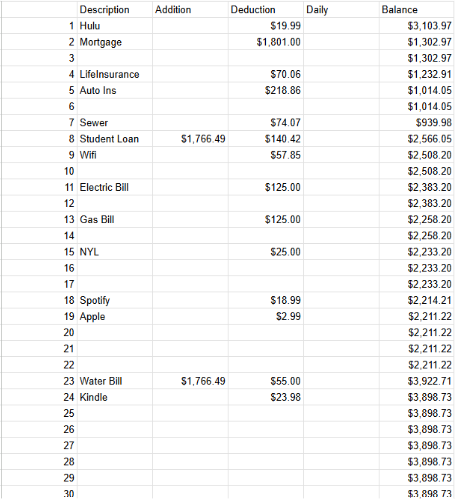

Scheduling with budgeting is writing down your fixed expenses and fixed income and what dates that money will come in and when that bill needs to be paid. See the below for an example of this:

This is something similar to the type of budget schedule I would use in terms of scheduling my inflows and outflows.

I can see the inflows (addition) and outflows (deduction) as well as a description of the expenses and a rolling balance on the right-hand column that changes as money comes in or out. The empty column “daily” is what I would use to keep track of my daily expenses such as groceries, gasoline, or other expenses if I were using a debit card.

If you were to use a credit card, you would need to put the budgeted payment amount on the date it is due on the schedule, so you do not overspend.

What I do want to make clear is that I am NOT anti-credit card. I personally think credit cards can be great when utilized very effectively. Reality is, most of us will always have a credit score or have a home loan for a good portion of our lives. I would avoid credit cards with a fee, unless you are a big spender that can make those points exceed the fee which is a whole other equation that needs its own examination (business owners or people making in the upper 10% fall into this category).

Personally, I have two credit cards. One is my daily use credit card that specializes in points for groceries, gasoline, and going out to eat. My other credit card is an Amazon Prime Visa which gets me 5% off any Amazon purchase. The main thing about credit cards is to pay off your statement balance every month. I will have another blog post dedicated to credit cards for more information.

Your inflows on your budget will be any income you make that goes into the bank. If you get cash that you plan to keep in your wallet, then do not put that income on this sheet. That money is not in your bank account, so do not put it in here. Likewise, if you spend that cash on something, do not post it on this sheet. This sheet is strictly for keeping track of your bank account balance.

Likewise, any outflows that occur through this account, which are usually your fixed expenses (bills and debt payments), need to be put on this sheet so you can be aware of your account having enough money in it to cover those debts.

If you do not have enough money in your account to cover that payment, you will more than likely, depending on your bank, receive an overdraft fee which is an additional expense that will deplete your account as well. It is a lose-lose situation and is a prime reason for why keeping track and scheduling out your expenses is so important.

I do find it interesting that there is some form of "budgeting" in the Bible. Now of course, there is not a book about budgeting or about how to lower your Netflix bill by sharing it with your roommate. Life was much different back then. What the Bible does talk about is having enough of something, or having a plan, before partaking in that action. And that is what a budget it. It is a financial plan that we follow in order to be successful in our lives. The Gospel of Luke, chapter 14, verse 28, states "Suppose one of you wants to build a tower. Won’t you first sit down and estimate the cost to see if you have enough money to complete it?" That is what a budget is. It is sitting down and having to cut costs somewhere, if needed, and have the money to complete it.

God Bless

Bubba Miller

Comments