Life Insurance

- Bubba Miller

- Apr 18

- 5 min read

Like all kinds of insurance, people claim that life insurance is a scam. And to some degree, I can see where people are coming from. According to InsuredAndMore.com, only 1-5% of term life insurance policies are paid out. Here is the thing to think about though; of those policies that are paid out, what if that person’s family did not have that life insurance death benefit? That family is effectively losing half, or maybe all, of their family’s income when that person passes away.

If you do the math, it is safe to assume that around 200k people 40 and under with a family die every year. According to insuranceinformant.com, about 50% of people have a term life insurance policy. That would conclude that of those 200k deaths, only 100k received a death benefit and 100k did not.

Those 100k that did receive a death benefit, although they cannot bring back the person, at least have some kind of death settlement so they can continue to stay at the home they lived at and sustain some kind of life similar to what it was life with that person’s income. Conversely, the 100k that did not have life insurance, not only lose a loved one, but also will more than likely have to change their way of life. If they have a mortgage, they may need to move and price the home to sell so they can make money to move out. They may have to sell the financed car because they cannot afford it. A lot of terrible effects in addition to losing a parent or spouse.

Most workplaces that provide benefits to full time workers do offer employer paid life insurance. While this death benefit is helpful, it is only going to be 2-3x their salary. That is just simply not enough money for someone who was providing income to the household. That begs the question, how much life insurance should a person have? And who should have life insurance?

First, anyone can have life insurance. Whether you are single, married, or somewhere in between, life insurance is a great thing to have. If you are married, the spouse will more than likely need your income to survive. If you are single, but have a home or vehicle that is financed, the transfer on death for those assets should be the beneficiary of your life insurance policy so they do not have to take on additional debt in addition to the grief of your passing.

Whenever I worked at New York Life and State Farm, both companies calculated it very similarly. First, you need to calculate your debt amount. Cars, home(s), student loans, etc. Next, you need to have about 7-10x your income, so your family has that income available and will not have to change their mode of life.

For instance, let’s say someone makes $60k a year, has $30k in student loans, a $300k mortgage, and a car loan of $25k. The math would be (60k*10)+30k+300k+25k=$955k. At this point I would just round up to a $1M policy. This needs to be done for both people in the family. Even if one of the people stays at home, it would be best to at least get the debt amounts for their life insurance, which would be about $400k.

The most inexpensive way to get life insurance for these situations is term life insurance. Term life insurance comes in 10, 20, or 30 year terms. Some companies may offer longer terms, but these are the standard terms. The industry standard term is 20 years. Mainly because your way of life changes about every 20 years. I also believe anytime someone buys a home (financed), they should look into reupping their life insurance as well.

Another hypothetical. If someone gets married at 25, but they are renting, more than likely their life insurance amount will need to be 7-10x their income, their vehicle debt amount, and student loans if they have any. Then at 32 they purchase a home, their life insurance portfolio will need to be reevaluated. More than likely they make a better income, they now have a home loan, and maybe they paid off some other debt.

What are the pros and cons of term life insurance? I would say the main pro is the cost. You can purchase a $1M, 20-year life insurance policy, if your health is good, for around $40/month per person at 25 years old (probably even less). Over 20 years that would be just $9,600 in premium for the financial peace knowing if something happened, your beneficiary’s financial way of life will not change.

The cons of this type of policy is that it will not grow any kind of cash value. Also, once it expires, you must get a new life insurance policy, which could cost more money because you are older, but in theory your life insurance death benefit should be less because you have money in retirement and have paid down your debt. Another con is that you are never guaranteed insurability. If you were to get cancer or other potentially terminal diseases, you will not be able to get a new policy. The current policy you have cannot be canceled, but getting a policy after its expiration will be either very expensive or not possible.

Back to the cash value, life insurance is not supposed to be a main retirement vessel. It is supposed to be death benefit insurance before anything else.

Whole life insurance is the main kind of life insurance that can build cash value. But it is also much more expensive than term. A 25-year-old non-smoker in good health could get $500k of whole life insurance for about $150 a month depending on the provider. (I had this quoted for me in 2022 is why I know this amount).

Or you can pay $40 a month for 20 years of term insurance at $1M death benefit and then renew at 45 years old for maybe $60 a month but the death benefit would be $500k.

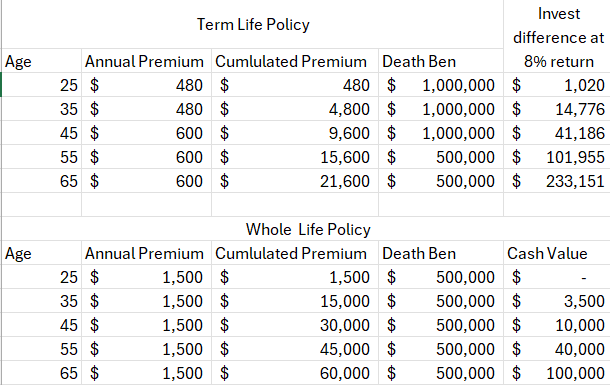

Below I took the liberty of comparing ways to structure life insurance for whole life and term life insurance. The whole life insurance cash value calculation was calculated by using an app called calculator.now online.

The annual premium for term life insurance is much lower than the premium for whole life insurance. So, what I did was invest the difference between the whole life insurance and the term life insurance into a hypothetical Roth IRA and assumed an 8% return which is consistent with the market.

As you can see, having term life insurance and investing the difference is a much better way to structure your insurance and retirement portfolio because it allows you to have a good death benefit while also having a good retirement account in addition to a 401k you should be investing in as well.

Ultimately, the choice is yours. If you have any questions, please contact a trusted life insurance provider in your area.

God Bless,

Bubba Miller

Comments