Introduction to Financial Statements for Personal Finance

- Bubba Miller

- Apr 11

- 4 min read

Understanding financial statements is not strictly for the businessman or businesswoman. Rather, understanding a financial statement is integral for someone to understand their current financial position. Whenever I was in college, my finance professor explained to us that a financial statement is a snapshot of where a company, or persons, finances are at that point in time, or the dates covered in the title of the statement(s).

My main focus will be on personal finances due to the style of this blog, so I will be omitting the statement of retained earnings and the income statement from this post. The two main financial statements I will go over will be the balance sheet and the statement of cash flows. A balance sheet is very good for seeing someone’s net worth and statement of cash flows is integral for creating a good budget.

At the end of the two explanations of the financial statements I want to do a fake case study of someone who makes “x” amount of money and has “y” expenses with “z” debt amounts. I think visualization is much easier for the human mind to comprehend vs words. I also think writing something down is much easier and effective to comprehend as well, so I do encourage people to complete their own B.S. and S.O.C.F. on their own whether it be on a computer or notebook paper.

First, I want to discuss the statement of cash flows. Statement of cash flows is strictly a financial statement that shows the money coming in and the money coming out. Essentially it is a budget without dates on it. It is strictly showing money coming in and money coming out. It is a pretty simple financial statement

Next is the balance sheet. The balance sheet shows someone’s assets and liabilities to calculate their equity. The mathematical equation is assets - liabilities = owner’s equity.

Assets contain essentially anything with value. There are three categories of assets.

Current (Short-Term) Assets: Items that are, or can be, converted into liquid cash within a year without penalty.

Cash

Cash Investments

Bank Accounts

Supplies (for a regular person, this is stuff you can sell)

Intermediate Assets: This is a current asset that can be converted to liquid cash, but it does incur a penalty. These are supposed to have more of a permanent nature than a liquid nature but can be liquid if needed.

Cars (the penalty is the sale value is less than you always think)

Retirement Accounts

Long-Term Assets: These are items that cannot be converted to liquid cash in less than a year. They are assets of a more permanent nature.

Land

House

Buildings

Liabilities are debt. That is the simplest way to put it. I also have categories for liabilities.

Current Liabilities: Financial liabilities that can, or should be, satisfied within a year.

Credit cards

Personal loans

Payday loans

Back taxes due under a year

Non-current liabilities: Financial liabilities that will be satisfied longer than a year.

Auto loans

Student loans

Back taxes due over a year

Home loan

Land loan

Retirement account loan

Owner’s equity is pretty simple. Assets (the things you own) subtracted by liabilities (the things you owe) is your equity. Owner’s equity is what you are worth. If your equity number is negative that means your debt exceeds your assets and vice versa means your assets exceed your liabilities, which is obviously what you want.

Scenario

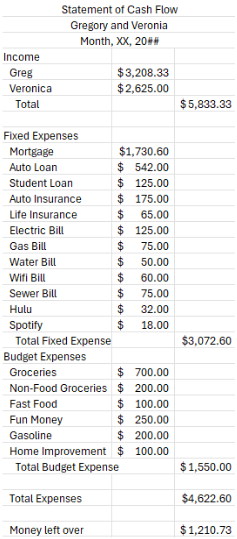

Greg is 28 years old and makes $55k.

Veronica is 27 years old and makes $45k.

They have no kids but are wanting kids here soon.

They bought a home 2 years ago for $250k and put 20% down after living below their means after college.

Greg’s vehicle is paid off.

Veronica has a car loan. They bought her a vehicle for $30k and put $6k down (20%). The term of the contract is a 4-year term at 3.9% (they have good credit). The payment on a $24k vehicle note is $542/month.

Greg has $20k in student loans and his payment is $125/month on a 20-year term.

Also, they both have retirement accounts. Greg has $15k in his 401k. Veronica has $10k in her 401k.

They are paid twice a month on the 15th and 30th.

Greg’s take home is $3,437.50 and he pays for the insurance for the family.

Veronica’s take home is $2,812.50.

Both of them contribute to their company 401k.

Statement of Cash Flows

Balance Sheet

I like this exercise for one of two things. One reason is that it shows what those two financial statements are and with the scenario involved makes them easier to explain. The second reason I like it is that it shows that the DINK stage of life is the time to save money and get yourself primed for your SIK stage of life. DINK is Double Income No Kids and SIK is Single Income w/ Kids. Obviously, you can always have a DIK life (Double Income w/ Kids) if you want to, but from a lot of people I have spoken with, the desire for a traditional familial lifestyle is returning and/or is desired. And I do think it is possible if you can be intentional earlier in life and also be intentional with your current financial statements and be intentional with a budget.

I mention the term intentional a lot in my blog posts. I think I mention that a lot because that is what can be a differentiator in a lot of aspects of life. Financial intentions, being intentional with your relationships, and being intentional in spiritual life. As the great Dr. Tim Crowley told a leadership class I joined “You have to slow down to speed up.” I have learned that is so true; when you slow down and are more intentional, you are less likely to mess up and more likely to encounter success in many aspects of life.

God Bless

Bubba Miller

Comments